Hard Assets Investor: Why has copper held its price so well while other industrial metals seem to have taken a hit?

Wing: Well, if you were talking to my boss [CEO] Frank McAllister, he would say that copper is the fifth precious metal. But let me set that aside and say that I think my understanding of it links to the dynamics of the world economy.

If you went back to around 1900 and you looked at the intensity of copper use in the United States, you would see that it was rising very steeply at that point. And that intensity of use, say, per unit of GDP or something like that, was indicative of the fact that the United States was industrializing at that point. Copper demand had grown and was growing very significantly. And, by the way, if you looked at the price of copper in 1910 compared to today in real dollars, it was up around $8 a pound, up substantially from where it is now [about $4 a pound].

In the 1930s, you not only saw the Great Depression, but you also saw the completion of that major industrialization phase in the U.S. The intensity of copper use dropped off in the U.S. It came back, to some extent, during World War II. Following the war, you saw similar spikes in intensity of copper use in Japan and in Germany. That was the rebuilding of those economies.

And then prices fell off somewhere around 1970 and languished from the early 1970s until the early 2000s, about 2003. And all of a sudden, you see another major economy starting to emerge at that point. And that obviously is China, and, to a lesser extent, some other countries. Underlying the strength in the copper price is the fact that China is still very actively industrializing. There is a lot of demand for copper coming out of there.

The demand for copper is exceeding the supply and is probably on trend to do that for a while, or at least is tight against supply. Copper is looking good for the next decade or 15 years, maybe.

HAI: Let’s talk about platinum. What’s driving demand in platinum right now?

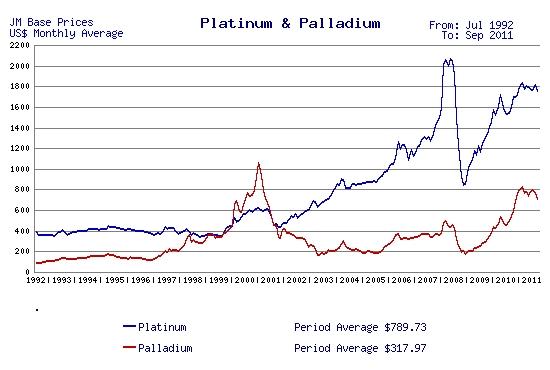

Wing: If you look at platinum — and this is true of palladium as well — there aren't very many places in the world where you produce significant quantities of platinum. South Africa produces probably 70 percent. Russia, as a byproduct, produces 20 to 25 percent. And the balance sort of comes out of companies like us. That’s just about it. So, on the supply side, there aren't huge tracts waiting to be developed. The cost curve drives platinum. In South Africa, the marginal producers are right up against the cost curve. On top of that, you’ve got the South African political scene, where people are talking about nationalization. It’s just really tough to make those investment decisions. And then you’ve got limited electricity and limitations on water. In effect, you’ve got platinum pretty well locked against the cost curve.

Obviously, palladium is the principal metal in gasoline catalytic converters. There still is a lot of platinum used in diesel catalytic converters, and a little more than 50 percent of European production is diesel. So that market is there.

The other growing application is in big on-road and off-road diesel applications, both stationary source and construction equipment, over-the-road diesels. So there’s some growth in demand there. And again, platinum supply isn't growing.

HAI: What is the recycling percentage a year of supply?

Wing: It’s probably about 1 million to 1.5 million ounces a year, on top of about 6 million ounces of native production.

HAI: So less than 20 percent?

Wing: That’s right. Others said they can see that going up to 2 to 2.5 million ounces over the next, well, let’s say five to 10 years. Hard to tell, exactly.

HAI: What about palladium?

Wing: Palladium is kind of a parallel story. The big producer, 50 percent or so of the market on palladium production is Norilsk Nickel of Russia. They produce it as a byproduct of nickel. The South Africans produce it as a byproduct of platinum. And obviously we produce it, and North American Palladium produces it, and, to a limited extent, the nickel producers in Canada produce some of it as a byproduct. And again, that’s about it, other than recycling.

The Russian angle to palladium isn’t discussed much. When Norilsk Nickel started large-scale production, which would have been around 1940-41, they also produced palladium as a byproduct. But in those days, there wasn’t really any market for palladium. So they stockpiled it until the fall of the Soviet Union. And estimates, at that point, had about 30 million ounces of palladium sitting in that stockpile.

When the Soviet Union became the Russian Federation and opened up to a freer market structure, the government began gradually selling off that inventory. They never quite said publicly how much is in that inventory. But just kind of working backwards, we’ve estimated that it’s somewhere between 25 and 35 million ounces. Since those sales began, about 30 million ounces have come out. Not much has come out in the last 18 months to two years.

There have been statements by Norilsk and by Russian Finance Ministry officials without attribution that that resource is about gone. The Russian agency that’s responsible for those sales came out earlier this year and said, “We are going to be selling some in 2012 as well.” But they also commented that, to do that, they would be reprocessing to get it up to quality.

Also, China is becoming key to the palladium story. Obviously, at the end of 2008, you saw worldwide auto production fall off fairly steeply. It’s been gradually recovering. In 2010, it was — on a worldwide basis — at record levels: somewhere around 75 million vehicles produced. And the big growth is not in the U.S. or America and Western Europe, it’s China. China is now the largest-producing and the largest-consuming country of vehicles in the world.

HAI: Does China have the same requirements for catalytic converters as the U.S.?

Wing: The requirements are a little bit lighter. But all vehicles produced there have to have catalytic converters. The engines probably, on average, are a little bit smaller. The requirement for platinum and palladium is a little bit lower, and in particular, palladium, because they're mostly gasoline catalytic converters. But again, the projections are that by 2015, we could be producing 100 million vehicles in the world; a one-third increase over where it is today. And obviously, that dynamic suggests that, against limited supply, price is attractive over time. I would quickly add that we think those underlying long-term dynamics are significant. But that’s not to say there won't be cycles in the price superimposed on top of that supply/demand dynamic.

HAI: What do you think of this new catalytic converter that uses gold?

Wing: Well, to the extent that technology is available to study, we’ve looked at it. It looks like it primarily is displacing a certain amount of platinum. At today’s prices, with gold right sort of neck-and-neck with platinum, I'm not sure there’s a whole lot of economic advantage to it. It doesn’t do very much to palladium, at least as we understand it. It’s mostly the platinum that it affects. And the platinum in gasoline catalytic converters is a pretty small component. It would be less than 5 percent.

Elsewhere, platinum production in South Africa is subsidised via lower energy prices (which are even below generation costs).